This guide will help you navigate the process of securing a long-term loan for major purchases in the Rio Grande Valley. Whether you’re looking to buy a home, land, or invest in property, understanding your financing options is crucial. You’ll learn about various loan types, the application process, and tips for boosting your chances of approval. To dig deeper into land financing, check out What You Need to Know About Texas Land Loans. Let’s get started on securing your dream investment!

Understanding Long-Term Loans

The significance of long-term loans cannot be overstated when it comes to making major purchases. These loans are specifically designed to span an extended period, typically over five years, allowing you to finance substantial investments such as homes, vehicles, or education. Understanding the ins and outs of long-term loans can help you make informed decisions tailored to your financial situation.

What is a Long-Term Loan?

Now, let’s probe into what constitutes a long-term loan. Generally, these loans are characterized by their extended repayment periods, which can range from several years to even decades. This longer duration makes monthly payments more manageable, which is particularly beneficial when considering major purchases that may exceed your immediate budget.

Moreover, long-term loans often come with relatively low-interest rates compared to their short-term counterparts. This makes them an attractive option for borrowers who need a significant amount of time to repay their debts, allowing you to plan your finances better while securing the necessary funds for your purchase.

Types of Long-Term Loans Available

Now that you have an understanding of long-term loans, let’s explore the various types available to you. Some common forms include mortgages, auto loans, student loans, and personal loans. Each of these options has unique features that may make them more suitable depending on your specific needs and financial situation.

- Mortgages: Typically used for purchasing real estate

- Auto Loans: Designed for financing vehicles

- Student Loans: For funding higher education

- Personal Loans: General-purpose loans for multiple uses

- Home Equity Loans: Leveraging your home’s equity for expenses

Assume that you need to purchase a home. A mortgage would likely be your primary option. However, if you’re looking to buy a vehicle, an auto loan would be more appropriate. Each type has specific characteristics that can work in your favor.

| Type of Loan | Typical Use |

| Mortgage | Buying property |

| Auto Loan | Purchasing a car |

| Student Loan | Education funding |

| Personal Loan | General expenses |

| Home Equity Loan | Utilizing home equity |

Long-term loans not only provide you with the financial backing required for major purchases, but they also spread out your repayment burden, making budgeting simpler over time.

Benefits of Long-Term Loans in Major Purchases

Long-term loans offer several advantages for financing your significant purchases. First and foremost, the capability to extend repayment periods means your monthly payments can be lower. This flexibility can alleviate some financial pressure, allowing you to allocate funds to other important expenses. Additionally, the fixed interest rates associated with many long-term loans shield you from rising rates over time, bringing predictability to your financial planning.

Long-term loans also provide more time for you to improve your credit standing while paying off the loan. This extended period can allow you to build a solid payment history, which can positively influence your credit score and make future borrowing easier and more affordable.

Loans obtained for major purchases through long-term financing can not only fulfill immediate needs but also help you cultivate long-term financial health. By managing repayments effectively, you can enhance your credit status, which may open doors for more advantageous loans down the line.

Assessing Your Financial Situation

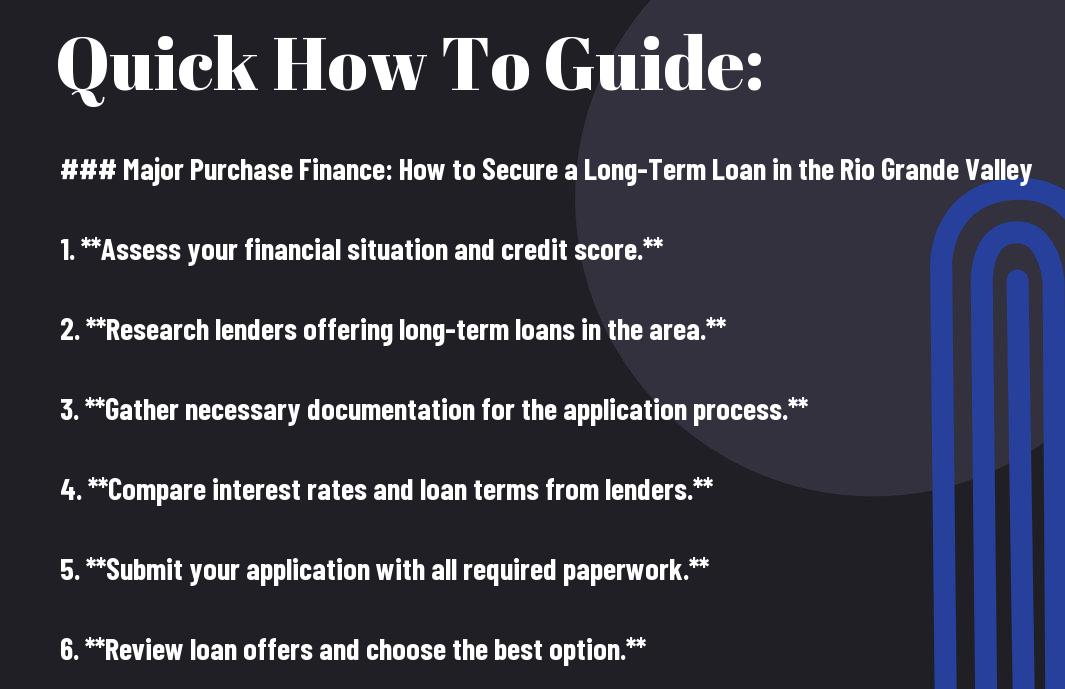

Assuming you are considering a long-term loan for a major purchase, the first step is to assess your financial situation thoroughly. Understanding where you stand financially will help you make informed decisions and secure the best possible terms for your loan. This includes evaluating your credit score, understanding your debt-to-income ratio, and determining your overall budget for the purchase. Each of these factors plays a crucial role in your borrowing power and the interest rates you may be offered.

Evaluating Your Credit Score

On your journey to securing a long-term loan, the first metric you should evaluate is your credit score. This three-digit number, typically ranging from 300 to 850, is a reflection of your creditworthiness. Lenders use your credit score to assess your risk level; the higher your score, the more likely you will qualify for advantageous loan terms. It is important to pull your credit report and review it for any discrepancies or negative factors that could impact your score. If you find inaccuracies, dispute them promptly to safeguard your financial standing.

On top of reviewing your current score, you should take proactive steps to improve it if necessary. This can involve paying down existing debts, ensuring all bills are paid on time, and avoiding new credit inquiries before applying for your loan. The healthier your credit score, the better your chances of accessing favorable loan conditions in the Rio Grande Valley.

Understanding Debt-to-Income Ratio

To truly comprehend your financial health, you must evaluate your debt-to-income (DTI) ratio. This ratio divides your monthly debt payments by your gross monthly income, allowing lenders to see how much of your income is already committed to debt repayment. A lower DTI suggests you have more disposable income available for a new loan, which increases your attractiveness as a borrower. Ideally, a DTI of 36% or lower is often recommended; however, many lenders may consider ratios of up to 43% acceptable, depending on your credit profile.

Understanding your DTI is crucial not only for loan approval but also for determining how much you can realistically afford to borrow without becoming overextended. To calculate your DTI, sum up all your monthly debt obligations, including credit cards, student loans, and any existing loans, and divide that total by your gross monthly income. Recognizing where you stand financially empowers you to make educated decisions regarding loan applications.

Score some extra points by aiming to reduce your DTI before applying for a long-term loan. You might consider paying down smaller debts or strategically refining your budget to enhance your income. Each percentage point can significantly influence lender perceptions, helping you to secure favorable financing options.

Determining Your Budget for Major Purchases

Credit assessments and DTI calculations are important, but ultimately, determining your budget for major purchases is where the rubber meets the road. This involves compiling all your potential expenses, from the loan repayment itself to related costs such as taxes, insurance, and maintenance. Being realistic about your finances means carefully evaluating your current income, expenses, and the additional financial obligations that a major purchase might entail. This way, you can establish what’s feasible and avoid falling into a debt trap.

Determining a budget not only ensures that you’re prepared financially but also helps you understand what options you can comfortably afford. Set clear limits based on your financial situation to guide your purchasing decisions effectively. Budgeting is an integral part of the planning process, setting the foundation for how much you can realistically borrow and pay back without jeopardizing your financial well-being.

Major purchases often come with unforeseen costs that can impact your finances for years to come. Therefore, it’s wise to leave room in your budget for potential expenses aside from the purchase price itself. This includes warranty expenses or emergency repairs, for instance. Careful budgeting prepares you not only for the purchase but also for sustained ownership, ensuring a smooth experience in the long term.

Factors to Consider When Securing a Loan

All major purchases often come with the need for a significant financial investment, and securing a long-term loan is a pivotal step in this process. As you venture into the world of financing, it’s necessary to weigh several factors that can influence your experience and overall satisfaction with the loan. Here are some key elements you should consider:

- Interest Rates and Loan Terms

- Lender Reputation and Reviews

- Loan Fees and Hidden Costs

Knowing these factors will empower you to make a well-informed decision and secure a loan that aligns with your financial goals.

Interest Rates and Loan Terms

If you’re seeking a long-term loan, one of the first things you’ll need to assess is the interest rate being offered. Interest rates can vary widely based on your credit score, the type of loan, and the lender you choose. A lower interest rate can significantly reduce the total cost of your loan over its lifetime. Additionally, you must consider the loan terms; this includes the duration of the loan and whether it is fixed or variable. A longer repayment term may mean lower monthly payments but can also lead to higher total interest costs.

Moreover, it’s necessary to understand the implications of different loan structures. Some loans may provide a greater degree of flexibility with payment options, which can be beneficial if you anticipate changes in your financial situation down the road. By carefully comparing these aspects, you can target a loan that fits your budget and future plans.

Lender Reputation and Reviews

Any lender you consider should have a solid reputation in the financial community. A lender’s track record, customer service, and transparency regarding terms and conditions play a crucial role in your loan experience. Before committing to a loan agreement, take the time to read reviews from current and former clients, as these can provide valuable insights into the lender’s reliability and practices. Look for patterns in feedback, especially in terms of communication and the handling of loan disputes, as this could impact your experience.

Loan approval processes can vary based on the lender’s practices, so choosing a reputable institution might save you from potential frustrations. Pay attention to their responsiveness and willingness to assist you in navigating the complexities of the loan process.

Loan Fees and Hidden Costs

Reviews of loan products often highlight the importance of recognizing all fees associated with your loan. These fees can include origination fees, closing costs, and prepayment penalties, which may not always be immediately apparent. It’s vital to obtain a detailed breakdown of all associated costs to avoid financial surprises down the line. Understanding all potential fees will help you negotiate better terms and select a lender that offers transparency.

Terms regarding fees can vary significantly, so being diligent in your research can yield substantial savings. Many borrowers overlook these hidden costs until it’s too late, leading to more significant debts than initially anticipated.

How to Prepare for Loan Applications

Now that you’ve decided to take the plunge into securing a long-term loan, the next crucial step is preparation. A well-structured approach significantly increases your chances of a successful application. This preparation phase primarily involves gathering pertinent information and documents, improving your credit score, and calculating what you can afford. Each of these steps plays a vital role in guiding you through the financing process and ensuring that you’re ready to make a sound financial commitment.

Gathering Necessary Documentation

Any potential lender will require specific documentation to assess your financial situation and eligibility for a loan. Start by collecting important documents such as your income statements—like pay stubs, tax returns, and employment verification. Additionally, you’ll need to have a record of your existing debts, including credit card statements, car loans, or any other financial obligations. This information will help lenders gauge your financial stability and ability to repay the loan.

Don’t overlook the importance of proof of assets, such as bank statements and any property you own. Having all your documents organized and accessible will not only smooth the application process but also reflect your seriousness and preparedness to potential lenders.

Improving Your Credit Score Before Applying

If you want to secure a favorable loan, enhancing your credit score before applying is crucial. Your credit score serves as a key indicator of your financial responsibility, and a higher score can lead to better loan terms, including lower interest rates. Start by reviewing your credit report for any discrepancies or errors that may need correcting. Pay off outstanding debts, especially those with high balances, and aim to reduce your credit utilization ratio by keeping your credit card balances low.

Moreover, be sure to make all your payments on time. Late payments can significantly hurt your score and your chances of getting approved for the loan you desire. Building a consistent payment history can bolster your credit profile and make you a more appealing candidate for lenders.

Plus, consider diversifying your credit mix responsibly. If you only have credit cards, think about taking on an installment loan or making regular payments on a small personal loan. Diverse credit types can favorably influence your score, provided you manage them wisely.

Calculating Your Loan Affordability

Clearly, understanding your financial limits is imperative when applying for a long-term loan. Before you submit your application, take the time to calculate how much you can afford to borrow without compromising your financial status. Consider factors such as your income, current expenses, debt obligations, and emergency savings. This holistic view of your finances will provide you with a clearer picture of the loan amount that fits comfortably within your budget.

Utilizing online loan calculators can also be beneficial in determining monthly payments and interest rates based on different loan amounts and terms. Make sure to account for potential fluctuations in interest rates and ensure that your budget allows for these variations over the term of the loan.

Credit plays a significant role in this calculation as well. A higher credit score can qualify you for better repayment terms, thus affecting your overall affordability. If you secure a loan with a lower interest rate, it may increase your purchasing power, enabling you to consider a more fulfilling and beneficial loan amount.

Tips for Finding the Right Lender

Once again, securing a long-term loan requires careful consideration, especially when navigating the diverse lending landscape in the Rio Grande Valley. You will find it helpful to follow a few key tips to ensure you partner with a lender that meets your financial needs. Here are some imperative strategies to assist you in your search:

- Research local lenders and credit unions.

- Check online reviews and ratings.

- Compare interest rates and terms.

- Ask about fees and closing costs.

- Consider customer service and support.

- Verify lender credentials and licensing.

Knowing which lender is right for you can be the difference between a smooth borrowing experience and a financial dilemma.

Comparing Multiple Lenders

Finding the right lender is crucial to securing the best loan terms. Start by gathering information from a variety of lending institutions. The differences in interest rates, fees, and repayment terms can significantly impact your financial future. Create a comparison table to evaluate your options effectively:

| Lender | Interest Rate (%) | Loan Term (Years) | Fees ($) |

|---|---|---|---|

| Lender A | 4.5 | 30 | 1,500 |

| Lender B | 4.0 | 30 | 2,000 |

| Lender C | 4.25 | 20 | 1,000 |

Comparing multiple lenders not only gives you a clear overview of your options, but it also empowers you to negotiate better terms. Take the time to analyze the pros and cons of each potential lender to ensure you make an informed decision.

Understanding Different Loan Offers

To navigate the world of loans effectively, you need to understand the different offers available to you. Loan products can vary significantly in terms of interest rates, repayment periods, and fees. Make sure you grasp the full scope of what each offer entails before making a commitment. Consider items like fixed vs. variable interest rates and how those choices align with your financial situation.

This understanding is vital as it allows you to weigh the benefits and drawbacks of each loan option. For instance, a lower interest rate may come with higher fees, which could affect the overall cost of the loan. By analyzing these elements, you can find the best financial solution that fits your budget and long-term goals.

Negotiating Loan Terms

Finding the right loan involves more than picking an offer at face value. Don’t hesitate to negotiate the terms and conditions with your lender. This is particularly crucial in the Rio Grande Valley, where local lenders might be flexible on their rates and fees. When discussing terms, communicate your financial situation clearly and express your expectations. You might be surprised at how willing lenders can be to work with you.

Offers can often be adjusted based on your creditworthiness and financial history. Show your ideal lender that you are a responsible borrower, and be firm in your negotiations to arrive at a mutually beneficial agreement. The more prepared you are, the more likely you are to secure favorable conditions that align with your financial needs.

The Application Process Explained

Not every loan application is created equal, and understanding the process can set you up for success when securing a long-term loan in the Rio Grande Valley. With several financial institutions available to you, the application process might vary slightly but follows a general pattern that you can anticipate. By familiarizing yourself with the steps involved and avoiding common pitfalls, you can move through your application with confidence.

Step-by-Step Guide to Applying for a Long-Term Loan

Application for a long-term loan entails various steps, which can be simplified into a systematic approach. Below is a table detailing the steps you’ll need to follow.

| 1. Assess Your Needs | Determine how much money you require and for what purpose. |

| 2. Review Your Credit Report | Check your credit score and history to understand where you stand. |

| 3. Research Lenders | Look for financial institutions that offer long-term loans tailored to your situation. |

| 4. Gather Documentation | Compile the necessary documents, including proof of income and identification. |

| 5. Submit Your Application | Fill out your application accurately and submit it to your chosen lender. |

| 6. Wait for Approval | Be prepared for the lender to take time to review your application. |

| 7. Review Loan Terms | Once approved, carefully review the terms before signing the agreement. |

Application for a long-term loan can sometimes be fraught with errors that might delay the approval process or even result in denial. One major mistake to avoid is providing inconsistent or incomplete information on your application. Ensure that your personal information matches what is on your identification documents and financial records. Additionally, failing to disclose any debts or financial obligations can lead to issues down the line.

Common Mistakes to Avoid During Application

Application processes can often trip you up if you’re not careful about your details. One common mistake people make is overlooking the importance of understanding the loan’s terms and conditions. Many applicants rush into signing contracts without fully comprehending the implications of interest rates, monthly payments, or fees involved. Take the time to ask questions and clarify what you’re entering into.

Another prevalent error is neglecting to double-check your financial documentation. Missing or inaccurate documents can lead to significant delays or even application rejections. Keep a checklist of required documents and ensure everything is up-to-date and accurate before submission.

What to Expect After Submitting Your Application

What you can expect after submitting your application largely depends on the lender’s specific timeline and procedures. Typically, you may receive an acknowledgment confirming that your application has been received. Following this, the lender will conduct a thorough review of the information you’ve provided, which may include verifying your credit history, income, and employment status. During this time, they might reach out for any additional information or clarification.

Once the review process is complete, you will get notification of approval or denial. If approved, the lender will outline the loan terms, such as the amount, interest rate, and payment schedule, which you will want to review carefully before signing any agreements.

Mistakes in your application can lead to extended waiting periods or complications during the review. To mitigate this risk, ensure that all submitted documents are accurate and consistent, as discrepancies can cause unnecessary delays and could even jeopardize your chance of securing the loan you need.

Managing Your Loan After Approval

To effectively manage your loan after approval, it is crucial to establish a plan that ensures timely repayments while accommodating your financial situation. This is where a solid strategy can make a difference. Start by evaluating your monthly budget and determining how much you can allocate toward your loan payments without overstretching your finances. You may also want to explore how to save and pay for a big purchase to provide additional funds for repayment.

Creating a Repayment Plan

Even after your loan is approved, it’s crucial to create a comprehensive repayment plan. Start by outlining the total amount borrowed, interest rates, and the loan term. This will help you calculate your monthly payments and create a schedule for when each payment is due. Incorporating these figures into your budget allows you to visualize how the loan fits into your overall financial landscape.

Moreover, it’s wise to set aside a small emergency fund to cover any unexpected expenses. This practice can help you avoid missing payments and incurring penalties. By being proactive and planning ahead, you can mitigate potential financial stress as you move forward with your long-term loan.

Staying on Track with Payments

Approval of your loan sets the foundation, but staying committed to your payment schedule is where your discipline truly comes into play. Consider setting up automatic payments with your bank, which will help ensure that you never miss a due date. By doing so, you can build a positive repayment history, enhancing your credit score over time.

With the implementation of a digital reminder system, you can keep tabs on your payment due dates and avoid late fees. Utilize calendar alerts or budgeting apps that sync with your bank account. This visibility will help you stay on top of your financial commitments while maintaining peace of mind.

Refinancing Options for Lower Rates

Lower interest rates can significantly impact your overall payment obligations and can free up your budget for other important expenses. Within the first few months after your loan approval, watch the market trends closely. If rates drop, you might consider refinancing to secure a better deal. Consult with your lender to explore the best possible options available for your situation.

Understanding the various refinancing options can play a critical role in your long-term financial health. By maintaining an open dialogue with your lender, you can stay informed about potential deals and qualifications necessary for refinancing. Ultimately, a lower rate could translate into considerable savings over the life of your loan.

Conclusion

From above, you have learned the imperative steps to secure a long-term loan for major purchases in the Rio Grande Valley. Understanding your financial landscape, assessing your credit score, and preparing the required documentation are critical first steps. You should also familiarize yourself with the various loan products available in the region and consider working with local lenders who can provide tailored options that meet your unique needs. A comprehensive understanding of your options will empower you to make informed decisions that align with your financial goals.

Additionally, maintaining open communication with lenders and staying informed about current market trends can significantly enhance your chances of obtaining favorable loan terms. As you commence on the journey to make a major purchase, remember that being proactive, organized, and knowledgeable will serve you well. By utilizing the strategies discussed above, you can navigate the loan process with confidence, ensuring that you secure the financing necessary to achieve your goals in the Rio Grande Valley.

FAQ

Q: What types of major purchases can I finance with a long-term loan in the Rio Grande Valley?

A: You can finance a variety of major purchases with a long-term loan, including homes, vehicles, boats, and large appliances. Most lenders will require that the purchase is substantial enough to justify a long-term loan, typically over several years. It’s important to assess your financial situation and choose a purchase that aligns with your long-term financial goals.

Q: How do I determine the amount I can borrow for a long-term loan?

A: The amount you can borrow for a long-term loan depends on several factors, including your credit score, income, debt-to-income ratio, and the lender’s policies. To better understand your borrowing capacity, begin by checking your credit report, calculating your monthly expenses, and consulting with potential lenders to evaluate different loan options tailored to your financial situation.

Q: What documents do I need to provide to secure a long-term loan?

A: To secure a long-term loan in the Rio Grande Valley, you will typically need to provide documents such as proof of income (pay stubs, W-2 forms, or tax returns), details of your current debts and assets, a valid form of identification, and the purchase agreement for the item you intend to finance. Some lenders may also require a credit report to assess your creditworthiness before issuing the loan.

Q: What should I consider before applying for a long-term loan?

A: Before applying for a long-term loan, consider factors such as your credit score, overall financial health, and the terms of the loan including interest rates, repayment period, and any associated fees. It is also important to compare different lenders and loan options to find the one that best meets your needs. Financial advisors often recommend having a solid repayment plan in place to avoid defaulting on the loan.

Q: Are there any specific lenders in the Rio Grande Valley known for offering long-term loans?

A: Yes, several local banks, credit unions, and online lenders in the Rio Grande Valley offer long-term loans. Some well-regarded institutions include Texas Regional Bank, International Bank of Commerce, and local credit unions. It’s advisable to research each lender’s rates, terms, and customer service before applying. Additionally, seeking recommendations from friends or financial professionals can be beneficial in choosing the right lender for your financial needs.