Over the years, businesses in the Texas Rio Grande Valley (RGV) have faced numerous financing options, but two popular choices have remained: Merchant Cash Advances (MCA) and traditional bank loans. Understanding the pros and cons of each financing avenue is crucial for you to make an informed decision that best suits your financial needs. In this blog post, we’ll break down these options, helping you weigh the benefits and potential drawbacks of MCAs and bank loans, so you can choose the one that aligns with your business goals and cash flow requirements.

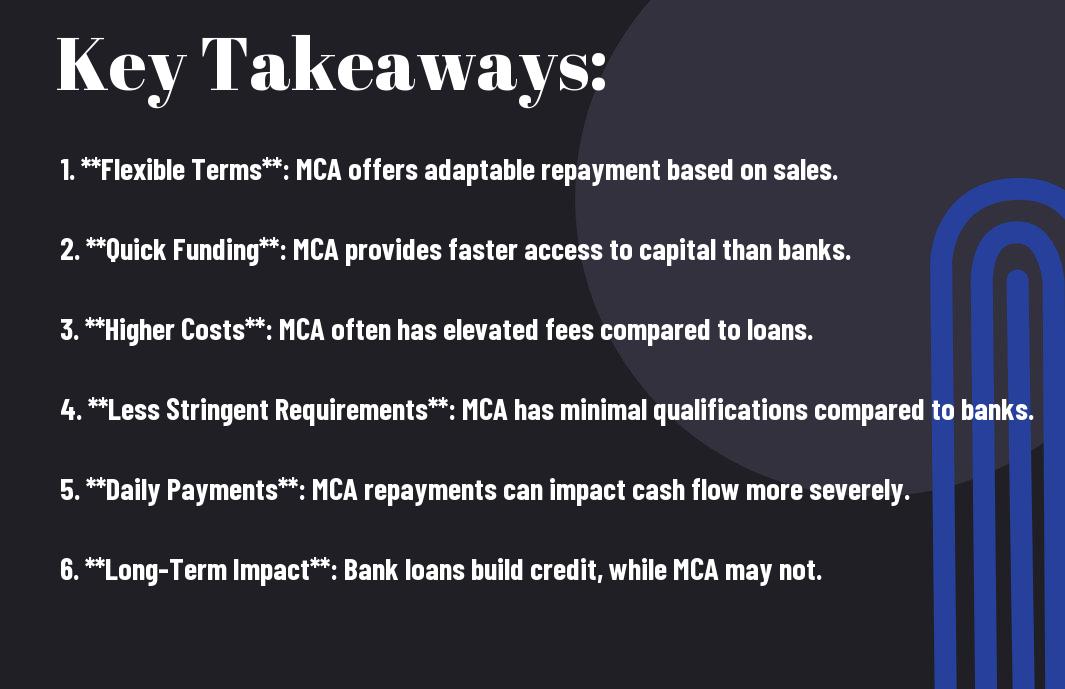

Key Takeaways:

- Accessibility: Texas RGV MCA loans are generally easier to obtain compared to traditional bank loans, making them a viable option for businesses with lower credit scores or those needing quick access to capital.

- Cost: While MCA may provide quick funding, the cost can be significantly higher due to higher fees and interest rates, which can impact overall profitability.

- Repayment flexibility: MCAs often have flexible repayment schedules that are based on daily sales, whereas bank loans typically require fixed monthly payments, which may be less accommodating for cash flow fluctuations.

Overview of Texas RGV MCA

To fully understand the benefits of Texas RGV Merchant Cash Advance (MCA), it’s crucial to examine into what it involves and how it operates within the financial landscape of businesses. The Texas RGV MCA program is designed to provide quick access to working capital for businesses facing cash flow challenges, allowing you to leverage future sales for immediate funding needs.

What is a Merchant Cash Advance?

Merchant Cash Advances are not traditional loans; instead, they are a type of funding where a lender provides you with a lump sum of cash in exchange for a percentage of your future credit card sales or revenues. Typically, this is a fast and flexible way to obtain money, making it an appealing option for businesses that need cash quickly.

With MCAs, you can access funds much faster than conventional financing routes since the application process is generally simpler and requires minimal documentation. This means that if your business is experiencing seasonal fluctuations or unexpected expenses, you can act swiftly to secure the capital you need to maintain operations.

Key Features of Texas RGV MCA

Merchant Cash Advances have unique features that make them particularly advantageous for small business owners in Texas. Understanding these key features is vital for making informed financial decisions. Below are the distinguishing characteristics of Texas RGV MCA:

- Quick access to capital, often within 24-48 hours.

- Flexible repayment structures based on daily credit card sales.

- Minimal paperwork and documentation required for application.

- No personal or business collateral typically needed.

- Suitable for businesses with fluctuating revenue streams.

The process is designed to cater to your needs, with repayment varying according to your sales, thereby reducing the strain during slower periods. This flexibility in payments can provide you with the financial leeway required to navigate unpredictability in your business cycle.

Differences between MCA and Traditional Financing

Traditional lending institutions typically require a thorough credit assessment, long documentation processes, and often require collateral to secure a loan. MCA operates under a different model, assessing your business’s cash flow and sales performance rather than your credit history. This difference often translates into a shorter approval time and easier accessibility for entrepreneurs in Texas needing immediate funds.

All things considered, while traditional financing options can take weeks and involve stringent requirements, Texas RGV MCAs offer a more straightforward solution that emphasizes your business’s present performance rather than its creditworthiness. This rapid access to funds is particularly useful for businesses with less-than-perfect credit histories.

Overview, the choice between MCA and traditional financing will depend heavily on your unique business situation, your need for immediate capital, and your ability to manage repayments based on sales fluctuations. Evaluating these aspects thoroughly will help you determine which option aligns best with your financial objectives.

Overview of Bank Loans

It’s important for anyone considering financial assistance to understand the options available to them. One common avenue for funding is through bank loans. For those in the McAllen area, you might explore the Best Personal Loans in McAllen, TX, which offer insight into various lending opportunities. Bank loans can come in various forms and cater to a range of financial needs, making it crucial to grasp their fundamental characteristics.

What is a Bank Loan?

With a bank loan, you are borrowing a specific sum of money from a financial institution with a structured repayment plan in place. The loan often includes interest charges, which are determined based on your creditworthiness. In essence, you receive a lump sum upfront, which you then repay over time according to the terms detailed in your loan agreement.

Bank loans can serve various purposes, including funding home purchases, paying for educational expenses, or consolidating debt. Understanding their mechanics and requirements can help you make informed decisions about your financial future and provide the funding needed for your aspirations.

Key Features of Bank Loans

The characteristics of bank loans can greatly influence your borrowing experience. Here’s a detailed look at the key features:

- Structured repayment plans with fixed or variable interest rates

- Interest rates based on creditworthiness

- Collateral requirements for secured loans

- Potential fees for late payments or origination

- Varied loan amounts and terms based on the type of loan

This diversity allows you to select a loan that aligns with your financial situation and goals. Many banks offer flexible terms, which can be beneficial in managing your finances. Keep in mind that your credit history will significantly affect the types of loans and interest rates you may qualify for.

Types of Bank Loans Available

What you’ll find is that various types of bank loans exist to cater to different financial needs. Below is an overview of some common types:

| Personal Loans | Unsecured loans designed for personal use |

| Home Loans | Secured loans specifically for purchasing homes |

| Auto Loans | Loans for purchasing vehicles, secured by the car itself |

| Student Loans | Loans tailored for education expenses, often with favorable terms |

| Small Business Loans | Funding solutions for business expenses and growth |

Types of bank loans may vary between institutions, so investigating the options available to you is crucial. Your needs dictate the type of loan that will work best for your situation.

- Understanding loan terms and conditions

- Evaluating interest rates and total payback amounts

- Considering collateral requirements for secured loans

- Identifying additional fees that may apply

- Researching lender reputation and customer service

After thoroughly exploring the diverse loan types and their features, you are better equipped to make an informed borrowing decision that suits your unique financial goals. It’s important to read through the terms provided by your lender to fully understand what you are committing to and how it will impact your financial well-being.

Pros of Texas RGV MCA

Once again, small businesses in the Texas Rio Grande Valley (RGV) have a valuable financing option available to them: the Merchant Cash Advance (MCA). Understanding the pros of an MCA can help you make informed decisions when considering financing solutions for your business. Below are some key advantages of Texas RGV MCA that set it apart from traditional bank loans.

Faster Access to Funds

Funds from a Texas RGV MCA can be accessed quickly, often within a matter of days. Unlike bank loans, which may take weeks or even months to process, an MCA allows businesses to receive cash almost instantly. This is particularly beneficial in times of urgent financial need, enabling you to seize opportunities or manage unexpected expenses without significant delays.

The streamlined application process for an MCA means that you can submit your documentation quickly, often requiring minimal paperwork. This efficiency helps you avoid the labyrinthine approval processes typical of conventional bank loans, allowing your business to move forward swiftly.

Flexible Repayment Terms

To many business owners, the flexibility of repayment options offered by Texas RGV MCAs is a game changer. Unlike fixed loan payments, merchant cash advances are typically repaid through a percentage of your daily credit card sales or other revenue streams. This means that during slower sales periods, your repayments decrease, alleviating some financial pressure.

The adaptability of these terms allows you to customize your repayment schedule according to your income flow, providing a level of comfort and ease in managing your business finances. With this flexibility, you can plan for both good times and bad, reducing stress when cash is tight.

The repayment mechanism can help you maintain your cash flow and manage expenses more effectively, especially for businesses facing seasonal fluctuations in revenue.

No Collateral Required

To secure a Texas RGV MCA, you typically won’t need to provide collateral, which can be a significant barrier with traditional bank loans. This means that your personal or business assets remain protected. Eliminating the requirement for collateral allows you to access funds without risking your hard-earned property, making it a safer option for many entrepreneurs.

Texas business owners can gain peace of mind knowing they won’t have to put their assets on the line to access necessary funds. This security is particularly relevant for startups or smaller businesses looking to grow without taking on substantial risk.

Ideal for Businesses with Fluctuating Revenues

The unique nature of an MCA makes it especially suitable for businesses that experience inconsistent income, such as retail shops, restaurants, and seasonal businesses. With repayment tied to sales, you won’t have to worry about meeting a fixed monthly payment when your revenues dip. This approach can safeguard your business during off-peak seasons, which many traditional loans do not accommodate.

This flexibility offers you a more manageable financial solution when times get tough, allowing you to devote more resources to critical business operations rather than stressing over rigid repayment schedules.

For instance, if your ice cream shop sees most sales during the summer months, you can benefit from the reduced repayment amounts during the slower winter months. This dynamism in repayments gives you the cushion needed to navigate seasonal ebbs and flows in business activity.

Minimal Credit History Requirements

An MCA often has more lenient credit requirements compared to traditional bank financing. This is particularly advantageous for new businesses or those with a limited credit history, allowing you to access funds without the stringent credit checks typical with bank loans. As a result, you can obtain financing even if your credit score isn’t stellar.

With less emphasis on credit history, this funding option opens doors for entrepreneurs who might otherwise struggle to secure financing. Texas RGV MCAs provide businesses with more opportunities to establish themselves and grow, regardless of their credit situation.

Cons of Texas RGV MCA

Many business owners consider a Texas RGV Merchant Cash Advance (MCA) as a quick and accessible financing option. However, it’s imperative to weigh the cons before making a decision. One of the main drawbacks of an MCA is often the higher interest rates associated with this form of financing.

Higher Interest Rates

Any time you consider taking an MCA, you should be aware that the interest rates can be significantly higher compared to traditional bank loans. This is primarily due to the increased risk that lenders take on when providing funds without collateral. As a result, your repayments could become a significant financial burden, negatively impacting your bottom line.

Moreover, the effective cost of borrowing through an MCA can be hard to quantify. Factors like the advance amount and repayment terms can obscure the actual interest rate you are paying, leading to surprises down the line. Thus, you should ensure that you fully understand the terms before committing.

Potential for Debt Cycle

One major concern with utilizing an MCA is the potential for falling into a debt cycle. As your business faces challenges in repayment, you might find yourself seeking additional funds from other MCAs or financing options, which can spiral out of control.

This cycle of borrowing can become detrimental, as each subsequent advance may come with even higher fees, making it increasingly difficult for you to catch up. The temptation to access more immediate capital can lead to a reliance on these advances rather than addressing underlying business issues.

With each additional advance, you may only be addressing temporary cash flow problems rather than solving the root causes, leading to a continuous need for borrowing and further complicating your financial situation.

Shorter Repayment Periods

With an MCA, you may also face shorter repayment periods than those typically offered through bank loans. This can put considerable pressure on your business, especially if cash flow is inconsistent. You may find yourself scrambling to cover daily operating costs while also ensuring you meet your advance repayment obligations.

Another important factor to consider is that the shorter repayment term can lead to a high percentage of your daily sales being siphoned off to service the debt. As a result, the availability of cash for operating expenses and growth opportunities can be drastically reduced, thereby hampering your business’s overall potential.

Limited Funding Amounts

One limitation of a Texas RGV MCA is the restricted amount of funding you can access. Unlike traditional bank loans that might offer substantial sums for large projects, MCAs generally have caps that may limit their usefulness for significant business expansions.

The smaller amounts offered can sometimes be inadequate for fulfilling more extensive financial needs, making you rely on multiple advances that can further compound financial pressure. It’s crucial to evaluate whether the available funding aligns with your business goals.

Impact on Cash Flow

Cycle repayments on an MCA can heavily impact your cash flow, which is vital for daily operations. The frequent deductions from your sales can leave you under financial stress, leading to difficulties in managing imperative expenses like payroll and inventory supplies.

Plus, if you’re already dealing with tightened cash flow, engaging with an MCA may only exacerbate your situation. The ongoing strain can limit your capacity to invest in growth opportunities or handle unexpected expenses, ultimately hindering your business’s long-term success.

Pros of Bank Loans

After weighing your financing options, bank loans often emerge as a favorable choice for many borrowers, particularly in the Texas RGV area. They present numerous advantages, making them a viable option for your business or personal needs.

Lower Interest Rates

Lower interest rates are one of the most appealing aspects of bank loans. Financial institutions typically offer competitive rates that are often lower than those associated with alternative financing options, such as merchant cash advances (MCAs) or credit cards. This means that over the life of the loan, you could save a substantial amount of money on interest payments, allowing you to allocate funds to other vital areas of your business or personal expenses.

Additionally, securing a bank loan can come with fixed interest rates, which provide predictability in your monthly payments and allow you to better manage your budget. This stability can be particularly advantageous when planning for future expansions or investments, as you won’t face fluctuating payment amounts.

Structured Repayment Plans

Structured repayment plans are another significant benefit of bank loans. These loans typically come with clearly defined terms, including the loan amount, interest rate, and repayment schedule, allowing you to plan your finances more effectively. This predictability can make monthly budgeting easier, as you will know exactly what to expect each month.

This structured approach not only helps you manage your cash flow but also ensures that you’re making steady progress in paying off your debt, which could enhance your financial stability. Having a consistent repayment plan can also aid you in avoiding the pitfalls of falling behind or incurring additional fees associated with less structured options.

Larger Loan Amounts Available

Bank loans tend to offer larger loan amounts compared to other financing methods. This can be a crucial factor if you’re aiming to finance a significant purchase, such as real estate, equipment, or extensive renovations. Banks assess your financial stability, credit history, and business plan to determine your eligibility for a higher loan amount, potentially allowing you to access the necessary funds for more ambitious projects.

Prospective borrowers often find that these larger amounts can provide the capital needed to make impactful investments that can contribute to long-term growth and success. Whether you’re expanding your business, purchasing property, or investing in major upgrades, having access to substantial funding through conventional bank loans can significantly streamline the process.

Builds Credit History

Pros of bank loans extend beyond immediate financial needs; they also enable you to build your credit history. When you take out a loan and consistently make timely payments, you contribute positively to your credit profile. This can enhance your credit score, which opens doors for better loan terms and conditions in the future. A stronger credit history also signals to lenders that you are a responsible borrower, making it easier to secure loans for larger projects or emergencies down the line.

The process of building credit through bank loans can be a vital component of maintaining financial health. A robust credit score typically results in access to lower interest rates and higher borrowing limits, aiding you in making further investments that can benefit your business or personal aspirations.

Potential for Additional Financial Services

Financial institutions often provide additional services to their loan customers, presenting you with more options for managing your finances. When you establish a relationship with a bank, you might gain access to more than just loans. Many banks offer services like financial advising, wealth management, and investment opportunities, all of which can help you make informed financial decisions.

Additional services can enhance your overall banking experience, providing guidance and resources to support your business growth or personal financial strategy. By utilizing these features, you can align your funding needs with a broader vision for your financial future.

Cons of Bank Loans

Unlike the more flexible financing options available, bank loans come with several drawbacks that may make them less appealing for your financial needs. If you are considering a bank loan, it is important to understand these potential disadvantages to ensure that you make an informed decision.

Lengthy Approval Process

On average, the approval process for bank loans can be quite lengthy. You may find yourself waiting several weeks, or even months, just to receive a decision on your application. This extended timeline can be frustrating, especially if you have immediate pressing financial needs or opportunities that require prompt funding.

Moreover, the drawn-out process can involve a significant amount of paperwork and bureaucratic red tape. As you navigate through endless documentation requirements and possible requests for additional information, you might find that your anticipated timeline for funding is pushed back further than expected.

Strict Eligibility Criteria

Eligibility for bank loans can be relatively stringent. Banks often require a strong credit score, a stable income history, and sometimes even a certain debt-to-income ratio that may rule you out. This high bar can be discouraging if you have less-than-perfect financial circumstances.

Loans through traditional banks are generally tailored for individuals and businesses that meet specific financial profiles. If you don’t possess the ideal credentials, your chances of securing a loan could be slim, or you may find yourself subjected to higher interest rates and less favorable terms.

Collateral Requirements

Lengthy loan processes at banks often include collateral requirements. Borrowers are typically required to offer assets as security to back the loan amount. If you cannot provide sufficient collateral, you may be denied funding altogether or compelled to seek smaller loan amounts that aren’t suitable for your needs.

Collateral serves as a safety net for the lender, which means that if you default on the loan, the bank can seize your assets. This requirement can be particularly daunting if you lack valuable property or assets to secure the loan, leaving you with limited options for financing.

Less Flexibility in Repayment

Any bank loan tends to come with rigid repayment structures. Most banks have fixed repayment schedules that require you to make regular payments over a set period. This lack of flexibility might not align well with your financial capabilities, particularly if your income fluctuates or if you face unexpected expenses.

To make matters worse, missing a payment can come with significant consequences, including fines, increased interest rates, or even damage to your credit score. Such strict repayment conditions can be particularly challenging for borrowers who may need modified payment plans to adapt to changing financial circumstances.

May Not Accommodate Urgent Financial Needs

Lengthy procedures, strict requirements, and rigid repayment plans mean bank loans often do not accommodate urgent financial needs. If you’re facing an unexpected emergency or a timely investment opportunity, waiting for a bank’s approval can lead to lost opportunities or heightened financial distress.

For instance, while you might need swift access to funds, the bank’s loan processes can be cumbersome and slow, potentially prolonging your need for financial relief. Consequently, your immediate needs may go unmet, making other, more flexible financing options more suitable for urgent situations.

To Wrap Up

Following this exploration of Texas RGV MCA and bank loans, it’s important to weigh the pros and cons carefully to determine which financing option best suits your needs. If you’re looking for quick funding with fewer qualifications, a Merchant Cash Advance (MCA) might appeal to you. However, be cautious of the higher interest rates and repayment terms that can strain your financial situation. On the other hand, traditional bank loans often offer lower interest rates, but the lengthy application process and strict eligibility criteria could pose a challenge for you, especially if you need immediate capital.

Ultimately, understanding the differences between these two options will empower you to make an informed decision based on your specific circumstances. You may want to consult with financial advisors or banking professionals to ensure you choose the best option for your business. For more insights, consider reaching out to Your Personal, Business and International Banking Partner in … for tailored financial solutions that can help you navigate this crucial decision.

FAQ

Q: What are the main differences between Texas RGV MCA and a traditional bank loan?

A: Texas RGV MCA (Merchant Cash Advance) is aimed at businesses that need quick access to funds with a repayment model based on daily credit card sales. In contrast, traditional bank loans offer a fixed amount to be paid back over a term but often require extensive documentation and credit checks. The MCA process is generally quicker and less formal than applying for a bank loan.

Q: What are the advantages of choosing Texas RGV MCA over a bank loan?

A: One of the main advantages of an MCA is the speed of funding, as businesses can often receive funds within 24-48 hours. Additionally, repayment is flexible and based on daily sales performance, which can ease cash flow concerns. There are fewer qualification requirements for an MCA compared to a bank loan, making it accessible for those with less-than-perfect credit.

Q: What are the disadvantages of Texas RGV MCA compared to bank loans?

A: The biggest disadvantage of an MCA is its higher cost; interest rates can be significantly higher than traditional loan rates. Also, the repayment structure can lead to faster depletion of cash flow since payments are taken as a portion of daily sales. Businesses relying heavily on credit card transactions could find themselves in a cycle of debt more quickly than with a standard loan.

Q: Who should consider using Texas RGV MCA?

A: Texas RGV MCA is ideal for businesses that have fluctuating cash flows or those that require urgent funding without the long wait associated with traditional lending. Retailers, restaurants, and service providers with a steady volume of credit card transactions can particularly benefit from this type of financing.

Q: What types of businesses are best suited for traditional bank loans?

A: Traditional bank loans are generally better suited for established businesses with strong credit histories, steady revenue streams, and solid operational stability. Businesses seeking larger sums of capital for expansion, equipment purchase, or long-term investments may find traditional loans more beneficial due to potentially lower interest rates and structured repayment terms.

Q: Can you use a Texas RGV MCA and a bank loan simultaneously?

A: Yes, businesses can utilize both an MCA and a bank loan simultaneously, but it is crucial to carefully manage overall debt levels. Having both financing options can provide more flexibility but can also complicate cash flow management. Businesses should assess their financial situation and ensure that they can meet the repayment obligations of both to avoid potential cash flow issues.

Q: How can a business decide which option is better for them: Texas RGV MCA or a bank loan?

A: The decision between Texas RGV MCA and a bank loan largely depends on the business’s specific needs, financial situation, and goals. Considerations include how quickly funds are needed, the total cost of financing, how predictable cash flow is, and whether the business can meet the qualifications for a traditional loan. Consulting with a financial advisor can also provide deeper insights tailored to the business’s unique circumstances.