RGV businesses often face tough decisions when it comes to financing options, especially when weighing the costs of merchant cash advances against traditional loans. Understanding the differences in terms of fees, repayment structures, and overall costs can be crucial for your financial health. In this blog post, you’ll discover the implications of choosing a merchant cash advance over a conventional loan, and how these choices can impact your business’s cash flow and growth potential in the Texas Rio Grande Valley.

Key Takeaways:

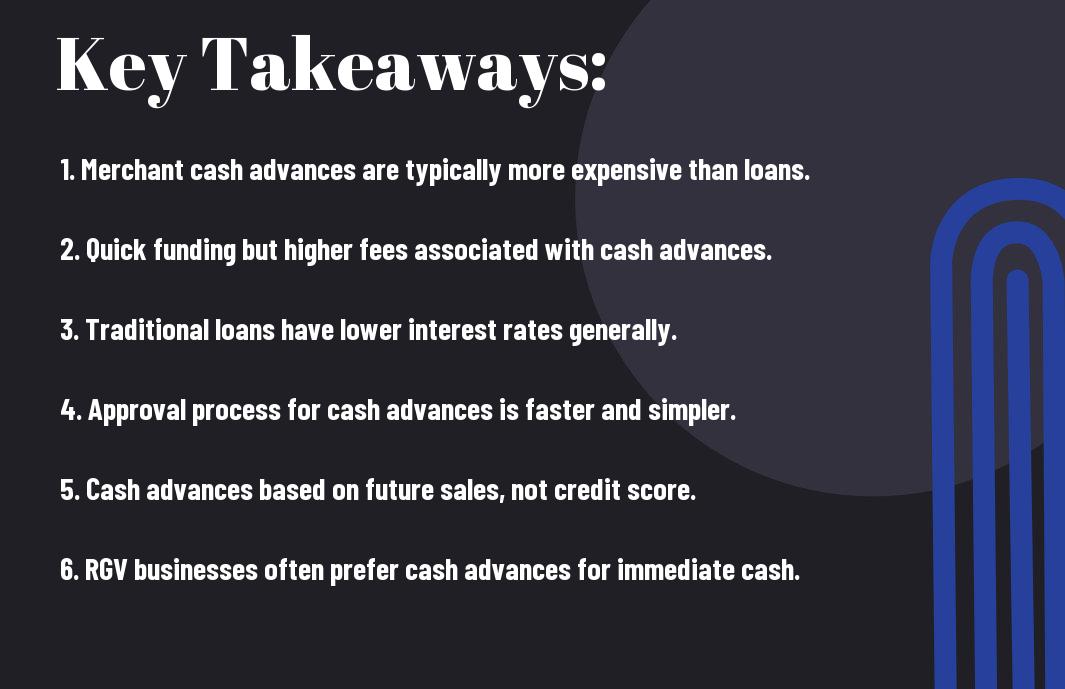

- Higher Costs: The cost of a merchant cash advance typically exceeds that of traditional loans, leading to higher overall repayment amounts for businesses in the Texas RGV area.

- Flexible Repayment: Unlike traditional loans, merchant cash advances offer more flexible repayment structures that can adapt to a business’s daily sales, which can be beneficial for seasonal or fluctuating revenue streams.

- Quick Access to Funds: Merchant cash advances often provide faster access to capital compared to traditional loans, making them a viable option for urgent financial needs in the Texas RGV market.

Understanding Merchant Cash Advances

Definition and Overview

To grasp the concept of a merchant cash advance (MCA), it is important to understand what it entails. An MCA is a financing solution that provides businesses with immediate cash in exchange for a percentage of future credit card sales or receivables. Unlike traditional loans that require collateral and extensive credit checks, MCAs focus more on the business’s sales performance, making them accessible to a broader range of entrepreneurs, especially those who may not qualify for conventional financing. This alternative funding option is particularly popular in industries with fluctuating cash flow, such as retail and hospitality.

On the surface, MCAs may seem straightforward, but they come with their unique set of features and implications that you should know. For example, the amount you qualify for is usually determined by your daily credit card sales, giving lenders a way to gauge your business’s performance. Additionally, repayment is typically automatic, as a portion of your daily credit card transactions is deducted until the advance is fully repaid. Understanding these elements is vital for making informed financial decisions.

How Merchant Cash Advances Work

Work by providing you with a lump sum of capital upfront, which is then repaid through a predetermined percentage of your daily credit card sales. This structure means that in periods of higher sales volume, your repayments will be larger, while in slower periods, your repayments decrease, easing the financial burden on your cash flow. This flexible repayment method can be particularly advantageous for businesses experiencing seasonal fluctuations in revenue.

Merchant cash advances typically involve a simple application process, often requiring only minimal documentation compared to traditional lenders. Once approved, you receive the funds quickly, sometimes within just a few business days. However, it is important to consider that calculating the cost of an MCA may involve a factor rate rather than an annual percentage rate (APR), making it crucial for you to understand how these costs are structured to avoid surprises later on.

Key Benefits of Merchant Cash Advances

To appreciate why many businesses opt for merchant cash advances, it’s important to look at the key benefits they offer. First and foremost, the speed of approval and funding is a significant advantage, allowing you to access cash almost immediately, whether it’s for emergency expenses, inventory purchases, or unexpected opportunities. Additionally, due to their flexible repayment structure tied to sales, you won’t feel as pressured during months when revenue may dip.

Merchant cash advances also cater to those who may have less-than-stellar credit scores or limited operating history, providing a lifeline to small business owners who could struggle to secure traditional financing. This inclusivity means that you can obtain the funds you need to grow your business without the strict requirements imposed by banks. Knowing these benefits can empower you to make better financial choices tailored to your situation.

Traditional Loans Explained

Clearly, it’s crucial to understand the fundamentals of traditional loans and how they differ from other financing options such as merchant cash advances. By grasping these concepts, you can make informed decisions about which financing route is best suited for your situation.

Definition and Overview

For anyone seeking financial support for their personal or business needs, traditional loans provide a structured approach to obtaining capital. These loans are typically offered by banks, credit unions, or alternative lenders, where borrowers are required to pay back the borrowed amount, plus interest, over an agreed-upon period.

| Feature | Description |

| Principal | The total amount of money borrowed. |

| Interest Rate | The cost of borrowing, expressed as a percentage of the principal. |

| Term | The length of time for repayment, usually in months or years. |

| Installments | Payments made regularly, usually monthly, to pay back the loan. |

| Collateral | Assets that may be used to secure the loan, reducing lender risk. |

Types of Traditional Loans

For your financing needs, traditional loans come in various formats, each designed for specific purposes and borrower profiles. Understanding these types can help you choose the option that best suits your requirements. Common types include secured loans, which require collateral like property or equipment, and unsecured loans that do not require any asset backing.

- Personal Loans: Unsecured loans for personal use, like medical expenses or education.

- Business Loans: Designed for business needs, these can be secured or unsecured.

- Mortgage Loans: Used for purchasing property, typically secured by the real estate itself.

- Auto Loans: Specific for vehicle purchases, secured by the car being financed.

- Credit Lines: Flexible borrowing options that allow you to borrow as needed, up to a limit.

This differentiation in traditional loan types allows you to pinpoint the best fit for your financial situation.

| Type of Loan | Purpose |

| Personal Loan | For individual expenses or emergencies. |

| Business Loan | For expanding or managing business operations. |

| Mortgage | For purchasing or refinancing real estate. |

| Auto Loan | For buying vehicles. |

| Home Equity Loan | Borrowing against home equity for cash access. |

Interest Rates and Terms

An important aspect of traditional loans is their interest rates and terms. These factors influence how much you will ultimately pay for the loan. Generally, interest rates are based on the financial institution’s assessment of your creditworthiness, prevailing market conditions, and the type of loan. You may find that more favorable rates are offered to borrowers with strong credit histories.

Additionally, the term, or the length of time you have to repay the loan, varies widely. It can range from a few months to several years, depending on the type of loan and lender. It’s crucial that you consider both the interest rate and the repayment term when deciding on a loan, as these elements significantly affect your overall cost and your monthly payment obligations.

Traditional loans are generally characterized by fixed or variable interest rates, which will determine how much you pay over time.

- Fixed-Rate Loans: Interest rate remains constant throughout the loan term.

- Variable-Rate Loans: Interest rate can fluctuate based on market conditions.

- Short-Term Loans: Typically have terms of one year or less.

- Long-Term Loans: Generally span several years for repayment.

- Prepayment Penalties: Some loans may charge a fee if you pay it off early.

This understanding of interest rates and terms is paramount to smart borrowing and effective financial planning.

Cost Comparison: Merchant Cash Advances vs. Traditional Loans

Not all financing options are created equal, especially when it comes to costs. When considering a merchant cash advance (MCA) versus traditional loans, it’s vital to break down the costs involved in each. The following table outlines the primary cost factors of both options:

| Cost Factors | Merchant Cash Advances | Traditional Loans |

|---|---|---|

| Interest Rates or Factor Rates | Higher, typically between 20%-150% | Lower, usually between 5%-20% |

| Repayment Structure | Daily or weekly deductions from sales | Monthly fixed payments |

| Overhead Fees | Minimal to none | Potentially high (origination, processing fees) |

| Approval Time | Days | Weeks or longer |

Analyzing the Costs of Merchant Cash Advances

To understand the true cost of a merchant cash advance, you need to consider both the factor rate and the repayment terms. MCAs generally use a factor rate instead of an interest rate, leading to an overall repayment that can significantly exceed the initial amount borrowed. Depending on your sales volume, the repayment structure, which is often taken as a percentage of daily sales, can either ease or exacerbate financial pressure. As a result, you must evaluate how this repayment method aligns with your cash flow to avoid sudden disruptions in your operational budget.

To put it into perspective, if your business experiences a dip in sales, you may end up repaying more than anticipated. Additionally, since MCAs do not require collateral, they can come with higher fees as lenders mitigate their risks. Therefore, understanding the total payback amount and how it meshes with your business’s sales cycle is crucial for making an informed decision.

Exploring the Costs of Traditional Loans

Cash is often king when it comes to traditional loans. These loans generally have lower interest rates compared to merchant cash advances, with a fixed repayment schedule that allows you to budget accordingly. However, traditional loans may come with additional costs such as application fees, origination fees, and other closing costs that can add up. It’s crucial to scrutinize these fees, as they can significantly affect the overall cost of borrowing.

Cash flow variability can complicate your finances if you are not prepared for the fixed repayment structure. Traditional loans often require a robust credit score and collateral, which can add additional hurdles to securing funding. While their lower rates appeal to many, the ability to meet repayment terms consistently is critical for maintaining financial health.

Cost analysis of traditional loans requires diligent evaluation of all related expenses. Be aware of fixed and variable costs, such as:

- Interest rates

- Application and origination fees

- Prepayment penalties

After meticulously calculating these costs, you can compare the traditional loan with alternative options like merchant cash advances to find the best financing method for your business.

Factors Influencing Cost Variability

Loans can vary based on several key factors that ultimately shape your financing costs. Your personal and business credit scores, the regulatory environment in Texas RGV, and economic conditions play a significant role in determining not just the interest rates but the overall cost of obtaining funds. Lenders assess perceived risk and adjust their offers accordingly. Therefore, it’s beneficial to improve your creditworthiness before applying for a loan or an advance.

Many small business owners overlook the impact of their business model, industry, and even the amount of the loan requested. For instance, high-demand industries may receive more favorable terms than others. Additionally, the terms you negotiate with the lender can significantly influence costs. Be aware of the different variables that might affect your specific situation:

- Credit scores

- Length of the repayment term

- Transaction history and cash flow

After understanding these factors, you can better anticipate potential costs associated with both merchant cash advances and traditional loans, assisting you in making a more strategic financing decision.

Cash advances can provide immediate funds but generally come with a higher price tag than traditional loans. Thus, carefully reviewing your financing options, including their costs and repayment structures, is imperative to safeguard financial stability within your business. Make informed choices to secure the best outcome for your financial health.

Eligibility Requirements

Now, when considering a financing option for your business, understanding the eligibility requirements for both merchant cash advances and traditional loans is crucial. Each type of financing has its own set of standards, so knowing what is required can significantly streamline your application process and help you make an informed decision.

Qualifications for Merchant Cash Advances

One of the primary qualifications for merchant cash advances is your business’s revenue. Lenders typically look for a minimum monthly revenue level, which can vary depending on the provider. While they may consider your credit score, they place more emphasis on your sales, which can work in your favor if you have a consistent cash flow. This flexibility allows you to obtain funds even if your credit history isn’t perfect, making it a viable option for many business owners.

Credit Score Considerations for Traditional Loans

Loans for traditional bank financing often hinge on your credit score, which is a critical component of the approval process. Generally, lenders prefer borrowers with a credit score of 680 or higher, as this indicates a reliable repayment history. Your credit score reflects not only your ability to pay back borrowed funds but also your overall financial health. A lower score can limit your options or lead to higher interest rates, impacting the cost of your loan.

With lenders closely monitoring credit scores, improving your score before applying for a traditional loan can increase your chances of approval and potentially secure you better loan terms. Factors influencing your score include payment history, credit utilization rate, and the length of your credit history. It is advisable to check your credit report for errors and to pay down any outstanding debts to bolster your score.

Documentation Needed for Approval

Considerations for documentation vary significantly between merchant cash advances and traditional loans. Generally, merchant cash advance providers require less documentation than traditional banks. While you might need to submit bank statements, proof of revenue, and a simple application, banks typically expect a comprehensive set of documents, including income statements, business plans, and tax returns, to assess your application’s viability thoroughly.

Credit requirements for traditional loans often entail a deeper investigate your financial history. The documentation you provide must clearly illustrate your business’s income, expenses, and overall financial stability to help persuade lenders of your repayment ability. Preparing this information can take time but is vital for ensuring you meet the stringent requirements of traditional financing.

Speed of Funding

For businesses in the Texas RGV, the speed of funding can significantly influence financial decisions. When time is of the essence, understanding how various funding options differ can help you make informed choices that align with your business needs.

Timeframes for Merchant Cash Advances

Speed is one of the standout features of a merchant cash advance (MCA). Typically, the funding process can take as little as 24 to 72 hours. After submitting your application and providing the necessary financial documentation, you can often receive approval quickly, which allows you to access the capital you need almost immediately. This quick turnaround is particularly advantageous for businesses that require urgent funding, such as those facing unexpected expenses or seasonal spikes in demand.

Timeframes for Traditional Loans

On the other hand, traditional loans usually involve a more extensive approval process. These loans can take anywhere from a few days to several weeks, depending on the lender and the complexity of your application. Lenders typically require a comprehensive review of your financial records, credit history, and detailed business plans, which can add significant time to the funding process.

Loans also frequently necessitate additional documentation and may involve multiple steps, such as appraisals or inspections, which can further extend the timeframe. In an environment where every day counts, the delays associated with traditional loans can hinder your business’s ability to respond to immediate opportunities or challenges.

Impact of Funding Speed on Business Operations

Impact is a vital aspect when considering the funding options for your business. The speed at which you can access funds affects not only the immediate financial needs but also your overall ability to operate efficiently. With an MCA, you can swiftly address cash flow gaps, seize sudden opportunities, or manage unexpected expenses without missing a beat. This agility can often be the difference between capitalizing on a fleeting opportunity or being left behind.

Timeframes play a crucial role in business operations. When you can rely on quick funding sources like merchant cash advances, you are better equipped to navigate the ups and downs of running a business. Conversely, the longer wait associated with traditional loans may force you to postpone necessary investments or operational initiatives, potentially leading to missed growth opportunities. Understanding these timeframes can help you select the right funding method that aligns with your immediate business needs and long-term goals.

Risk Assessment and Business Impact

Many business owners are drawn to the accessibility and speed of merchant cash advances. However, understanding the potential risks associated with these alternatives to traditional loans is vital for your business’s long-term health. One significant concern is the high cost associated with merchant cash advances, which can lead to an ever-increasing cycle of debt if not managed correctly. Furthermore, since these advances are repaid through daily debit card sales, fluctuating revenue can create uncertainty in your cash flow, potentially leading to financial strain.

Potential Risks of Merchant Cash Advances

Business owners often overlook the repercussions of relying heavily on merchant cash advances. The repayment terms, typically structured as a percentage of your daily sales, can significantly fluctuate based on your business performance. This arrangement means that in slower months, you could be left without sufficient cash to cover other operational expenses, creating a precarious financial environment. Additionally, if your business performs poorly, you may find yourself in a situation where debts spiral, leading to even harsher repayment terms.

Risks Associated with Traditional Loans

Loans can present their own set of risks, particularly for those who may already be experiencing financial strain. Higher interest rates and stricter repayment schedules can create a heavy burden, especially during unforeseen downturns. If you miss a payment, not only do you face late fees, but this can also negatively impact your credit rating, making it even more challenging to secure credit in the future. It’s imperative to weigh these consequences before deciding on a traditional financing route.

Assessment of your financial situation before applying for loans is crucial. For instance, if you have inconsistent revenue streams or have recently experienced losses, securing a traditional loan may prove difficult due to the perceived risk by lenders. This can further complicate your situation as you navigate through the application process and any resulting rejections can affect your business’s ability to grow.

Effects on Business Cash Flow

Risks associated with each financing option can significantly impact your business’s cash flow. A merchant cash advance, while providing quick access to funds, requires you to relinquish a portion of your sales, potentially hampering your ability to invest in growth opportunities. If your income is inconsistent, this arrangement could leave you scrambling for cash to cover other necessary expenses.

Potential consequences for your cash flow don’t just end with repayment models. For businesses considering traditional loans, maintaining adequate cash flow is equally as important. A failed loan application can mean needing to seek alternative and potentially more expensive financing options later. All of these factors make it imperative to carefully assess your financing choices and develop a strategy that aligns with your business’s operational needs. Understanding these dynamics is key to not only achieving financial stability but also ensuring long-term success.

Conclusion

Conclusively, understanding the cost implications of merchant cash advances compared to traditional loans is vital for your financial decision-making in Texas’ RGV. Merchant cash advances typically come with higher fees and less favorable payment terms, which can lead to rapid depletion of your revenue. While they may offer quicker access to funds and more flexible repayment options based on your daily sales, the long-term cost can be significant. It’s crucial for you to carefully evaluate whether the convenience of fast funding is worth the increased financial burden that might arise.

On the other hand, traditional loans generally present lower overall costs, longer repayment periods, and fixed rates, making them a more affordable option in the long run if you qualify. Understanding your financial situation and considering all available financing options allows you to make informed choices that align with your business goals. For a deeper explore the nuances between these financing methods, consider exploring Merchant Cash Advances vs. Traditional Loans and learn how each option can impact your business’s financial health.

FAQ

Q: What is a merchant cash advance (MCA)?

A: A merchant cash advance is a type of financing where a business receives a lump sum payment in exchange for a percentage of its future credit card sales or daily bank deposits. It is not classified as a loan, making it an alternative option for businesses that need quick access to cash, especially in Texas RGV, where businesses often face fluctuating cash flows.

Q: How does the cost of a merchant cash advance compare to traditional loans?

A: The cost of an MCA is typically higher than that of a traditional loan. This is because MCAs are considered a higher risk for lenders and usually come with a factor rate instead of an interest rate, leading to a more expensive total repayment amount. For example, while traditional loans might offer interest rates ranging from 5% to 25%, MCAs can have effective rates that equate to much higher costs, sometimes exceeding 100% APR when annualized.

Q: What are the primary factors that determine the cost of an MCA?

A: The cost of a merchant cash advance is determined by several factors, including the business’s credit card sales volume, the business’s overall creditworthiness, the repayment terms, and the factor rate offered by the MCA provider. Businesses in Texas RGV may find that local economic conditions also influence these costs, reflecting regional financing trends.

Q: Are there any specific fees associated with merchant cash advances?

A: Yes, MCAs can come with various fees, such as origination fees, processing fees, and early repayment fees. It’s important for businesses to read the agreement carefully to understand all costs involved. Unlike traditional loans, which often have clearly defined terms, MCA agreements can vary widely in their fee structures and total charges.

Q: Why might a business in Texas RGV choose an MCA over a traditional loan?

A: Businesses in Texas RGV might opt for a merchant cash advance due to the speed and ease of the application process, as they usually require less documentation than traditional loans and can be funded more quickly. Additionally, businesses with poor credit that may be ineligible for traditional financing might find MCAs to be a more accessible option, despite their higher costs.

Q: What are the risks involved with taking a merchant cash advance in Texas RGV?

A: The primary risk of a merchant cash advance includes the cost of repayment relative to the profit earned, as a failed repayment may lead to cash flow issues for the business. Additionally, if business revenues decrease, the repayment amounts can still be substantial, potentially leading to a cycle of debt. Small businesses in Texas RGV must carefully evaluate their cash flow forecasts before opting for an MCA.

Q: How can a business effectively manage the costs associated with an MCA?

A: To manage the costs of a merchant cash advance, businesses should create a comprehensive repayment plan that aligns with their expected cash flow. It’s also wise to explore multiple MCA providers to compare factor rates and terms, and to seek advice from financial professionals. Furthermore, maintaining strong credit and steady revenue can improve access to better financing options in the future, possibly transitioning to traditional loans that have lower costs.